Buying and owning an apartment in Singapore is easy, says no one ever. Whether you are a young, middle-income couple looking to move into a cozy BTO love nest or a Miss Independent realizing the dream of one groovy bachelorette pad, there is an encyclopedia of rules, legislations and financial obligations you need to sink your nose in before you take the plunge. The five quick facts we are presenting to you below will serve as your introductory course to homeownership in Singapore.

We are just as excited as you are about owning your very first home. Even if you have budgeted your war chest right down to each cent, you need to fulfill the eligibility criteria at the very least. For private property buyers, simply put, you would only have to be concerned about scouring the right bank loan package to finance your new condo apartment. For HDB buyers, it is a little more complex. But we’ll break down and simplify some of the primary criteria for you.

If you are single and looking for ways to finance your first home, check out this housing guides for singles in Singapore.

Let’s say you and your spouse have decided to own an HDB flat. Unfortunately, that is only the start of the many layers of decision making. The next big one you two have to make is whether to go for a new BTO flat or a resale. On paper, it seems there are more pros to buying a resale. You can choose from any location in Singapore and you don’t have to twiddle your thumbs for three years to collect your keys, but you do have to prepare to pay a premium known as Cash Over Valuation (COV). You are also responsible for negotiating for an agreed price between yourself and the seller.

BTO flats usually conduct launches every quarter and due to the fact that they tend to be developed in non-mature estates, chances are you get to relax a little bit on the affordability front. Nevertheless, you should still confirm and then double confirm whether you are truly ready to commit. Get an approval-in-principle from your bank to get a rough sketch of what you can expect to be paying over the course of the tenure.

For those on the BTO camp, the hot spots seem to be centered around the likes of Bidadari, Tampines, and Punggol. And if you haven’t already seen the HDB Awards 2016 finalists, a lot of the projects have been so exquisitely designed they can easily pass off as private condominiums.

But don’t hop on the hype just because everyone is flocking to the showrooms like some kind of tourist attraction. Spend a little more time to deliberate the distance to supermarkets, schools, your parents’ home, bus stops, and, of course, MRT stations. This is wrong you can’t right overnight.

Undoubtedly, the greater the convenience, the higher the house is going to cost you. Once a location feels absolutely right for you, don’t wait. You wouldn’t want to hold it off until the official opening of Downtown Line 3 and Thomson-East Coast Line drive the valuations higher than they already are.

Applicants of HDB concessionary loans (loan ceiling at 90%) can fund the 10% down payment, monthly repayments, and stamp duties using CPF OA. Under the staggered down payment scheme, that 10% is broken down to 5% payment over two sessions: one during the signing of the lease agreement, another during key collection. You don’t need to carry cold hard cash on hand. That’s right, HDB loans are good that way.

Takers of private bank loans are subjected to a loan ceiling of 80%, which means down payment is higher at 20%. Out of the 20%, at least 5% has to be made in cash. If you have a greater capacity to tackle the payments in cash, there are 60% and 40% loan quantum options. The reason why some folks swear by bank loans over HDB concessionary loans is that their flexible packages give them some measure of control against interest rate hikes. The interest rates on HDB loans are pretty much fixed, and that would render them less angelic when market interest rates are attractively low.

If you are taking up an HDB loan, you will have to apply for an HLE (HDB loan eligibility) letter which needs to be submitted during the signing of the lease agreement. It is valid for six months. Bank loan applicants will have to submit a letter of offer from the bank instead.

Applying for either an HDB or a bank loan is not a matter of right or wrong, black or white. It really boils down to how comfortable your finances are and whether it is well within your total debt servicing ratio (TDSR).

Learn more about choosing between an HDB or a bank loan.

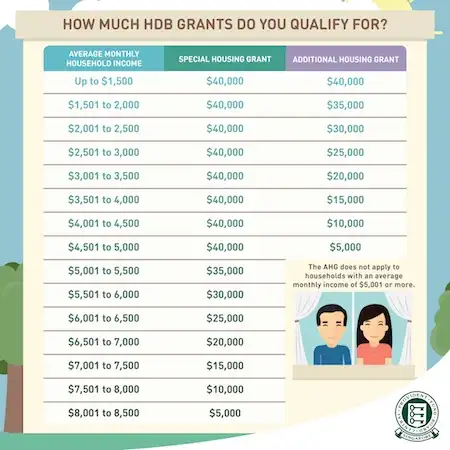

Picture credit: https://www.areyouready.sg/YourInfoHub/Pages/News-How-much-BTO-grants-do-I-qualify-for.aspx?utm_source=facebook&utm_medium=post&utm_campaign=bau

This picture is originally featured on Are You Ready?

This should sway you over to HDB ownership. First time flat buyers can apply for either the additional housing grant or special housing grant to offset the cost of purchase. Depending on whether you exceed the income ceiling for 2 to 4-room Flexi flats, you can qualify for up to S$40,000 in the grant amount. Assuming your new flat costs S$400,000, it’s as good as having your down payment settled by the lovely peeps at HDB.

This article was first published on GoBear Singapore blog.